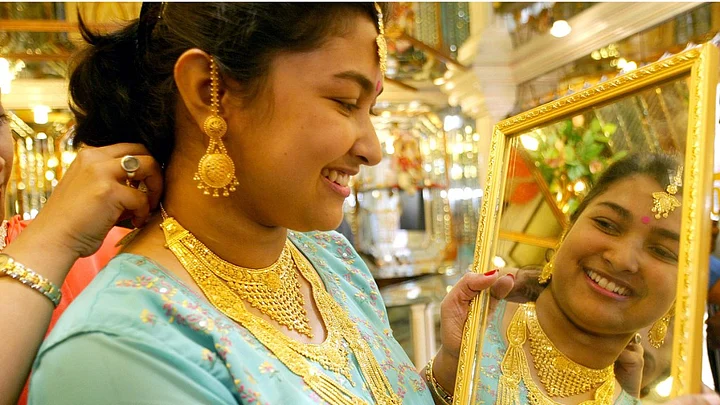

Younger Indians are falling out of love with gold.

The nation’s jewellers are struggling to attract more youthful customers, as cultural ties to gold weaken amid rapid urbanisation, greater access to other investments and the lure of high-end consumer goods.

“I remember my mom buying small rings for every Hindu festival throughout the year since childhood,” said 25-year-old lawyer Saloni Sulakhe. “But in our generation it’s completely unrealistic to be investing in gold when you’re just going to keep the gold to yourself,” she said, adding mutual funds are better because there’s no emotional value and you can sell them when needed.

Sulakhe, who moved to Mumbai about eight years ago from a town 400 kilometers away, has taken financial advice and prefers investing the bulk of her savings in funds and insurance policies. She has bought some gold because “all my life I have heard from my parents that gold is supposed to be a good investment,” she said in a telephonic interview.

Rupees earned by young urban professionals are also flowing to more regular vacations, better gadgets and other trappings of a wealthier lifestyle. The competition is forcing jewellers to adapt, via more modern designs, online purchases for their more internet savvy customers, and other sales offers that seem more akin to clothing or white goods retailers.

Titan Co, India’s top maker of branded jewellery by market value, has been selling urban-chic items targeting young women through its Mia brand since 2011 and bought a majority of online retailer CaratLane in 2016. Others such as PC Jeweller Ltd. and Tribhovandas Bhimji Zaveri Ltd have started selling their products on e-commerce sites like Amazon.com Inc and Flipkart Group.

Two-thirds of India’s 1.4 billion population are under 35, according to a Credit Suisse Wealth Management report. At the same time, the proportion of urban dwellers has risen to about a third, from a quarter in 1990, as citizens migrate to major conurbations and smaller towns expand. The long-term consequences for demand in the world’s biggest bullion market after China are stark.

India’s Fading Love Affair With Gold

India’s consumption of gold, almost all of which is imported, has been on a declining trend since 2010, because of the government’s efforts to curb its trade deficit and Prime Minister Narendra Modi’s crackdown on so-called black money that’s outside the official economy and has escaped taxation.

By contrast, investment funds under management had tripled to 22.6 trillion rupees ($330 billion) by May, according to the Association of Mutual Funds in India, from just 7.4 trillion rupees eight years ago, when gold demand in the country reached a record high of more than 1,000 metric tons.

The fading of India’s love affair with gold, an attraction that goes back centuries, removes another pillar of support from the international bullion market where prices have dropped to the lowest in more than six months.

Physical demand in places like India and China has sometimes helped establish a market floor as retail buyers step in when they think prices are relatively cheap. Gold steadied around $1,250 an ounce on Friday, a level Suki Cooper, a Standard Chartered Plc analyst, says has attracted such buyers in the past.

The bedrock of demand in India remains its poorer, rural population, who are ill-served by the banking system and where gold is the only savings option. That, coupled with the tradition of gifting jewelry at weddings and festivals, should keep purchases between 750 and 850 tons a year.According to Kumar Jain, owner of the UT Zaveri jewelry store in Mumbai’s Zaveri Bazaar

More educated customers are buying smaller pieces of jewellery for investment purposes, and not to wear, said Jain, a third-generation jeweller who’s grooming his 28-year-old son to take over the business. “Marketing strategies are changing and the way we operate is also evolving,” he said. “We are trying the online route, door-to-door sales, mailing design catalogs, and allowing customers flexibility in payment options.”

(This story was originally published on BloombergQuint.)

(At The Quint, we question everything. Play an active role in shaping our journalism by becoming a member today.)